Generally, an individual starts working after graduating and continues until the age of retirement. This is the cycle of life. Over the working years, people tend to save money so that they can put it to use in their grey years when the age is not on their side, and cash flow remains a concern after leaving work. Thus, a situation where you free yourself of financial liabilities and accumulate enough wealth for your retirement is known as achieving financial independence.

While we all know of this but not many

practices this, in our daily hustle-bustle, we do not devote time to financial

independence.

At this, let me ask you, is financial

independence a delusion?

Well, the answer is NO. It refers to the

state where an investor has enough resources to meet his/her expenses and to

fulfill his/her future financial goals.

You may be wondering if you can achieve

independence despite having a meager salary and high cash outflow towards

different bills. The answer is yes; it can be achieved. But would require careful

planning, timely review, and a high degree of patience. One important point to

highlight here is that more you delay, the most challenging it shall become to

achieve financial independence. Thus, a smart approach would be to get on to

the idea of savings from the early years of your career. Starting as early as

the first salary shall help you plan for other goals such as house, vehicle,

children’s education, electronic gadgets, foreign trip, and the likes.

Following are the steps an investor should ideally

follow to achieve financial independence.

Blog Index

Save and invest

An investor should start by saving a part of income. This can be done by making investing a habit every month. For this, you may always consider starting a SIP-based on different financial objectives such as buying a house, or retirement planning, and the likes.

Ideally, around a quarter of your monthly

income should go towards savings. This helps you in creating liquidity and also

helps in creating wealth.

How much can you make by opting for a SIP?

Well, this can be way higher than you

expect, all due to the compounding effect. That is why you should start at

least the SIP of your retirement, the moment you get your first check.

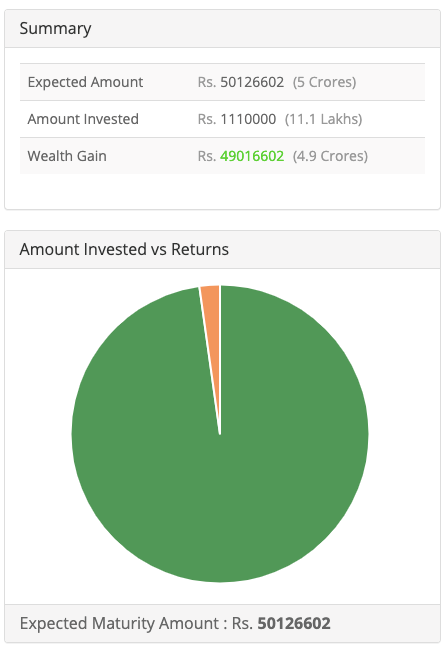

Suppose you invest Rs 2500 per month in a SIP that offers you an average annual return of around 15%. In this case, you end up accumulating Rs 5.01 crore in 37 years when you turn 60 at retirement (assuming you are 23 when you start working).

Source: SIP Calculator

A healthy dose of equity should be in the

portfolio

The equity asset class has offered

investors very healthy returns. This is the only asset class that has been

consistently generating positive returns and is beating inflation year on year.

Also, if an investor starts early and plans appropriately, the asset class has

helped in the accumulation of wealth, helping him/her achieve financial

freedom.

SIP makes sense if you can’t commit to

lumpsum

Don’t think that investment is only for the

rich who have high cash flow and liquidity. Even if you do not have a lump sum

or a very high surplus, you can still invest. There’s no harm in starting small

and making it big.

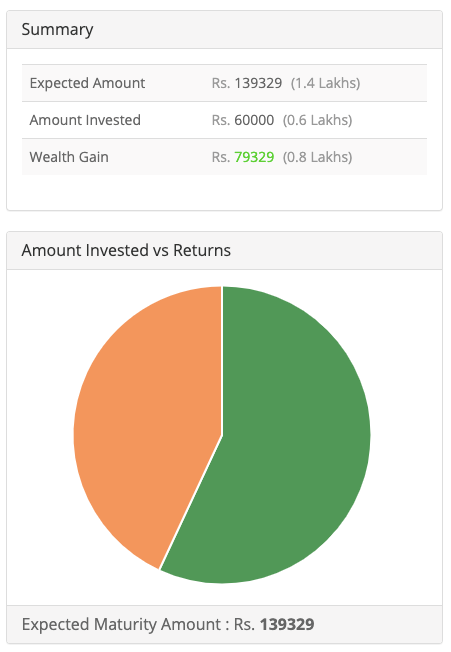

If you make a small SIP of even Rs 500 a

month in a fund that has generated 15% returns (average) in the past for ten

years, you will accumulate Rs 139329 – a broad 2.32 times over your investment

of Rs 60000.

Source: SIP Calculator

So, it can be seen that SIP is not about

the amount; it is about starting early and remaining invested for the

long-term.

Goal planning is important

We all have goals such as marriage,

retirement, travel, children’s education, buying a car, etc. You would agree

when we say that each of these goals or milestones would happen at different

times in your life. Thus, you are required to ensure you have a separate plan

for each.

Opting for one fund that would help achieve

all the goals isn’t a possibility as things may go against plan, particularly

in equities and in the short-term.

Process of financial independence

In India, more and more retail investors

are becoming aware of the benefits of SIP and thus are adopting the systematic

way of wealth creation to meet their goals. Amidst this, we believe educating

the lot with the process of achieving financial independence is the key.

Following are the broad guidelines that detail the process on how should an

investor plan –

Define your goals

The first step that helps you identify

where you intend to reach and by when.

Know your risk-taking appetite

Before you invest any penny, it is crucial

to know how much risk you can take. In simple words, the extent of loss (if it

happens) that will not shake your cash flow or will not impact you much is your

appetite.

Asset allocation

Asset allocation is nothing but the mix of

different asset classes such as gold, real estate, equity, and debt in your

overall portfolio. Optimal asset allocation is the mix of an asset class that

provides you maximum returns at a given level of risk. Given SIPs are generally

long-term in nature, you should be mindful of the fact that equities tend to

perform well over the long-term, and the asset allocation should be done

accordingly.

Select the funds

The final step of the investment process is

fund selection. With over thousands of funds, it gets difficult to scout for

the best that suits your requirements. At Tarrakki, we employ a detailed

process to select the fund that best suits your needs and allows you to reach

the goal efficiently.

To conclude, we can say that SIP is a powerful tool that has helped individuals accumulate wealth. The benefit of compounding that an individual gets by starting early in the life cycle is unmatched. Also, it is essential to note that an SIP can be started with a small amount that is as low as Rs 100 (for some funds, otherwise it is Rs 500 generally) and can run into few millions. In SIP, what matters it the horizon and how early you start and not the sum of money should you wish to accumulate wealth.

Should you wish to know more or are looking to take the first step, feel free to download the Tarrakki App – India’s most trusted brands for mutual fund investment. The app provides you with a very easy to use interface (similar to DIY) and helps you start your journey in less than 60 seconds.